Funeral Planning in the UK

Funeral Guide has worked with YouGov to commission a study into funeral planning. The results highlight the lack of funeral provision across the UK. With the cost of a funeral over £4,000, are bereaved families facing a debt crisis?

Key findings

- Only 6% of adults in the UK have a pre-paid funeral plan

- People in Wales are 50% less likely to have a funeral plan than other parts of the UK

- People who have never married are 4x less likely to have a funeral plan

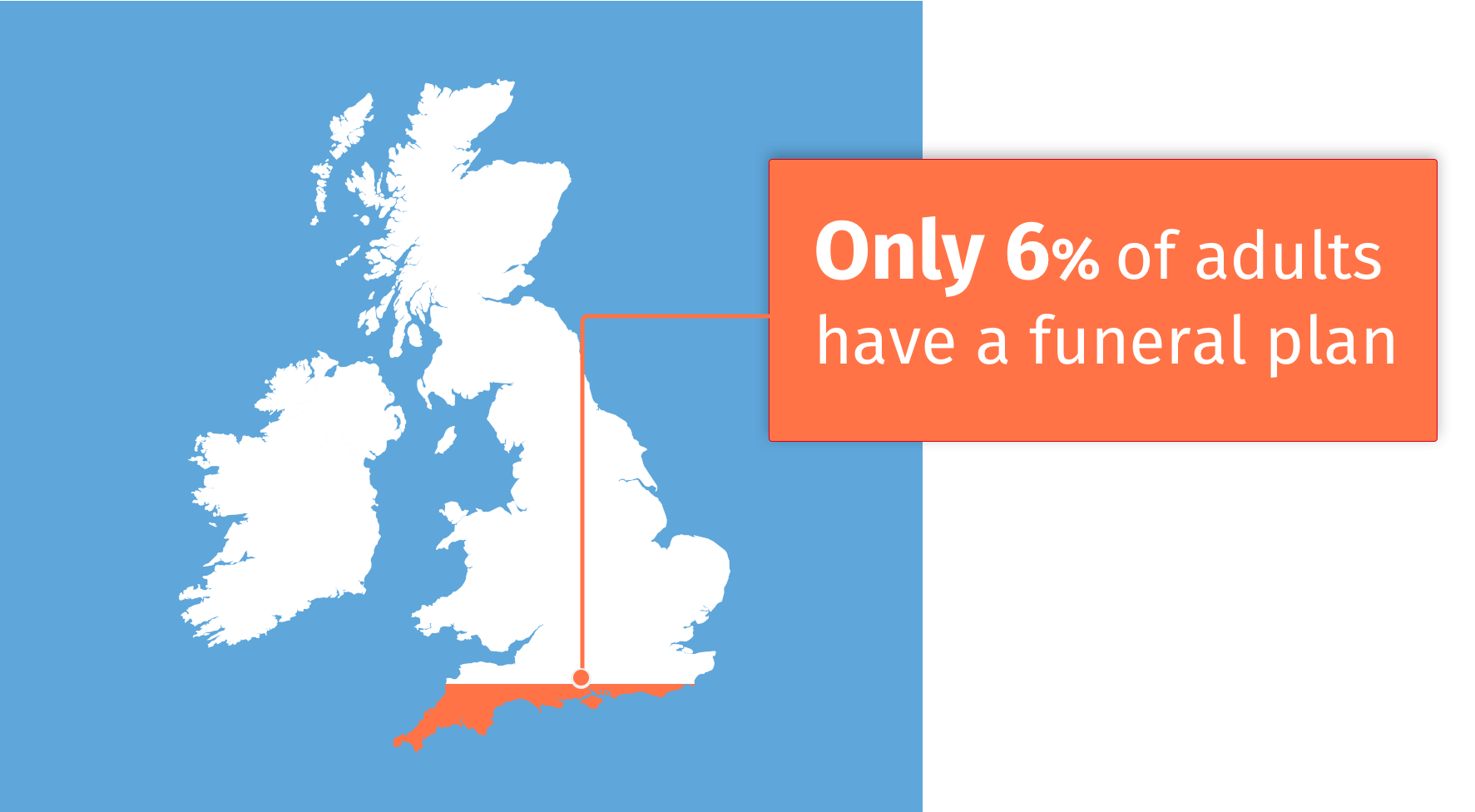

Results for the UK

Do you have a pre-paid funeral plan (e.g. in order to cover the costs of your funeral)?

When analysing the results for the UK, only 6% of adults have taken out a pre-paid funeral plan. This is in contrast to other European nations where end-of-life planning is much more common. In Holland, 70% of people have a funeral plan, whilst 20 million Spaniards have funeral insurance.

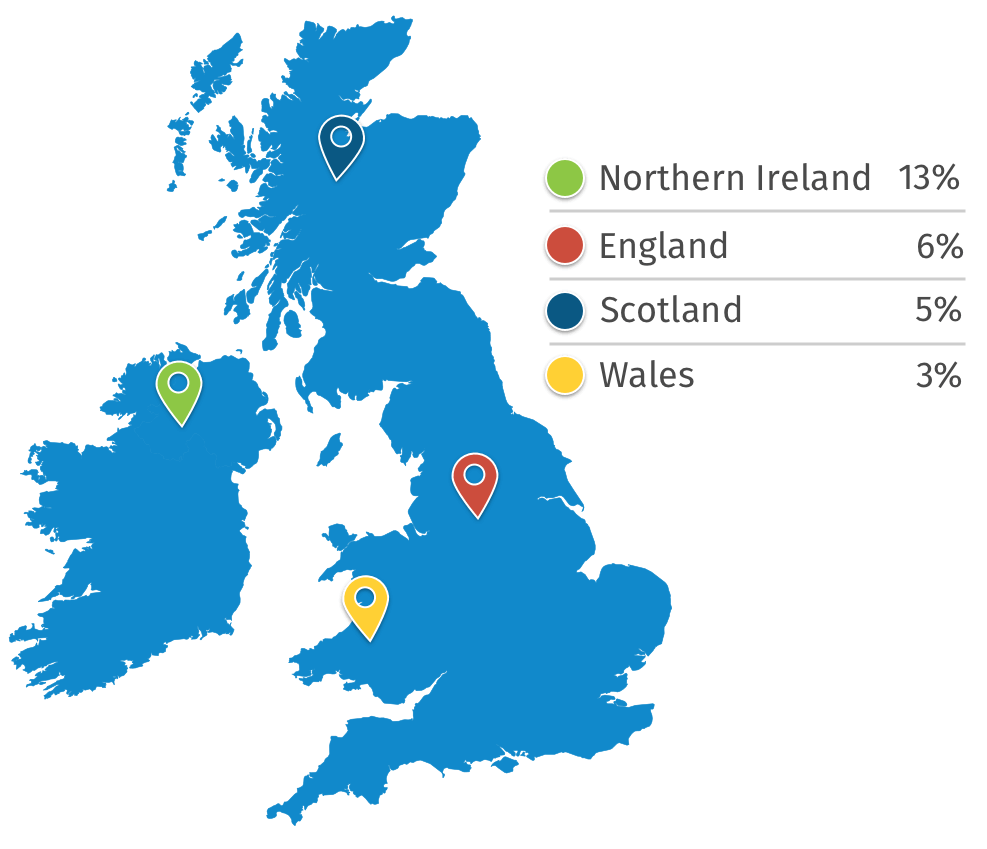

Results by region

Do you have a pre-paid funeral plan (e.g. in order to cover the costs of your funeral)?

When analysing the results by region, Northern Ireland stood out with 13% of those polled having a funeral plan in place. In comparison, the region with the lowest number was Wales, with only 3%. The results in Wales may reflect the widely-reported higher level of poverty in western Wales.

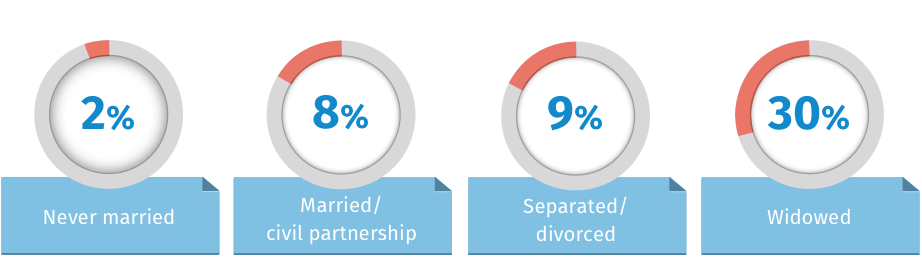

Results by marital status

Do you have a pre-paid funeral plan (e.g. in order to cover the costs of your funeral)?

When analysing the results by marital status, being unmarried means you are less likely to have planned for your funeral. Losing a loved one has a major impact on end-of-life planning, as those who were widowed are significantly more likely to have a funeral plan in place.

Other findings

- Only 2% of adults under the age of 55 have a funeral plan

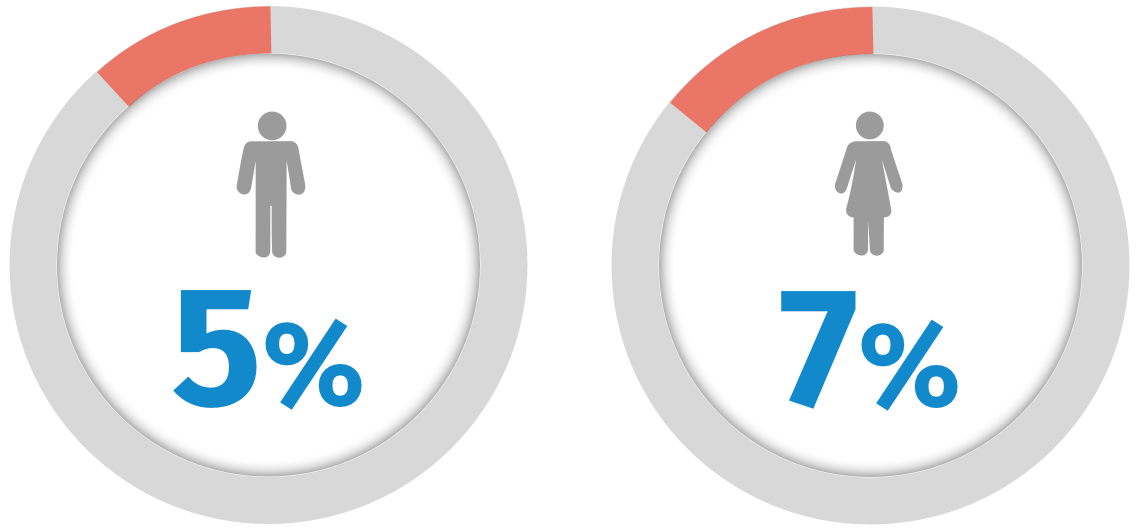

- There is relatively little difference between men and women taking out funeral plans

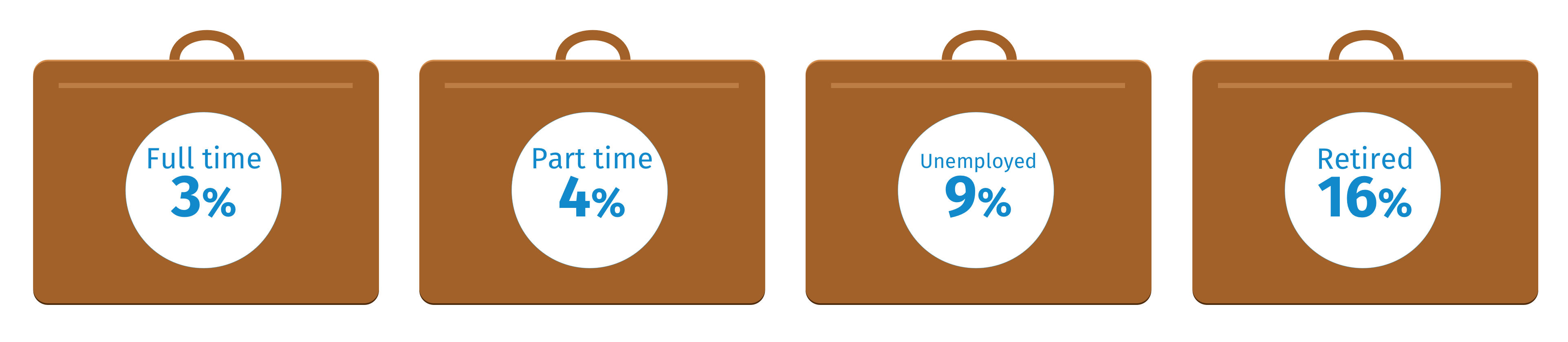

- Less than one in six retirees have a funeral plan

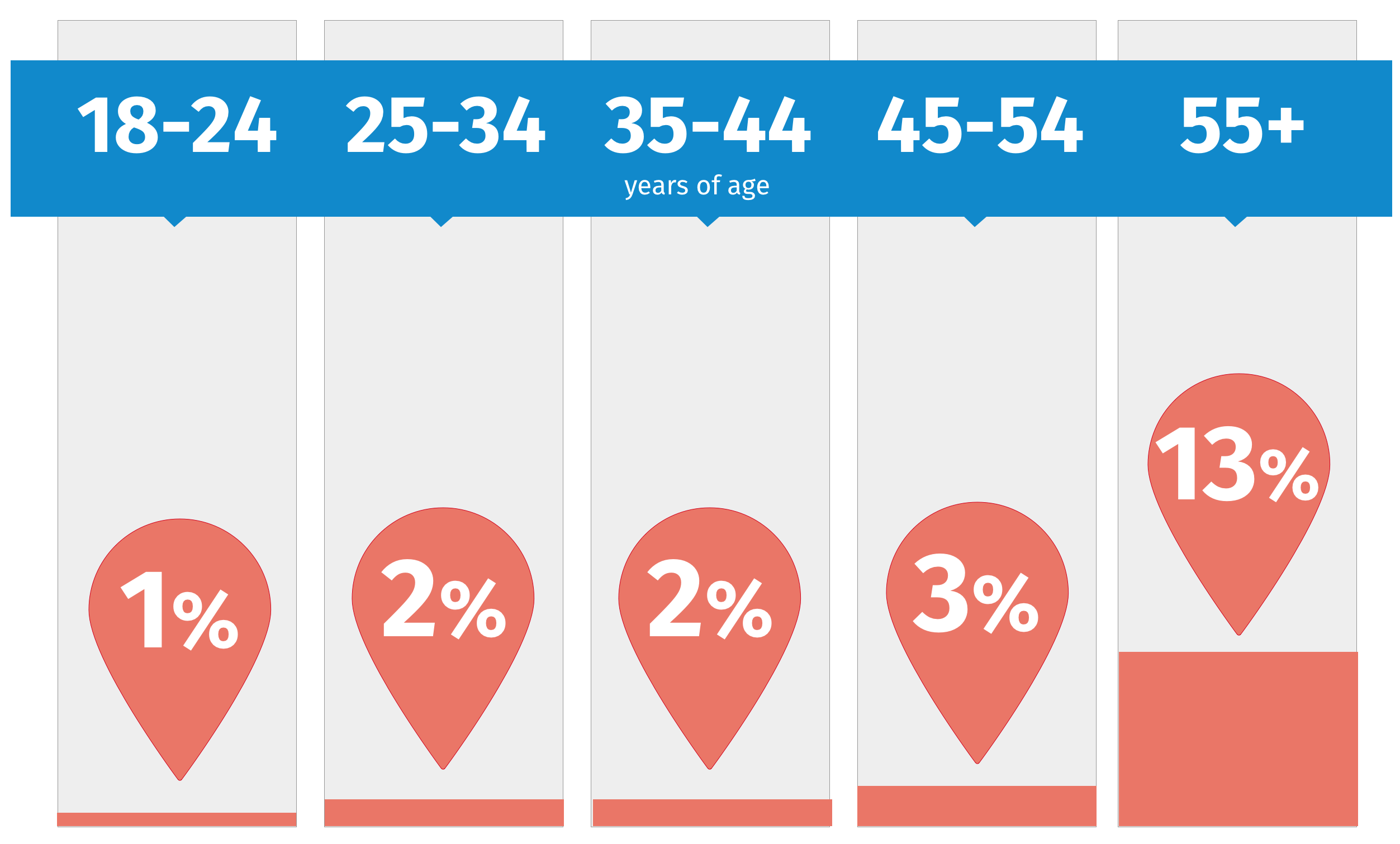

Results by age

Do you have a pre-paid funeral plan (e.g. in order to cover the costs of your funeral)?

When analysing the results by age, those in the 55+ age bracket were more likely to plan ahead. However, the percentage of this age group who had a funeral plan was still only 13%. Most worrying was the 45-54 age bracket where only 3% of respondents had planned for their funeral.

Results by gender

Do you have a pre-paid funeral plan (e.g. in order to cover the costs of your funeral)?

When analysing the results by gender, although a larger percentage of women had funeral plans in place, there was relatively little difference between men and women.

Results by income

Do you have a pre-paid funeral plan (e.g. in order to cover the costs of your funeral)?

When analysing the results by income, those that had retired were more likely to plan ahead. However, the percentage of retirees who had a funeral plan in place was still only 16%. This shows how few people are taking funeral plans seriously, even when end-of-life planning is essential.

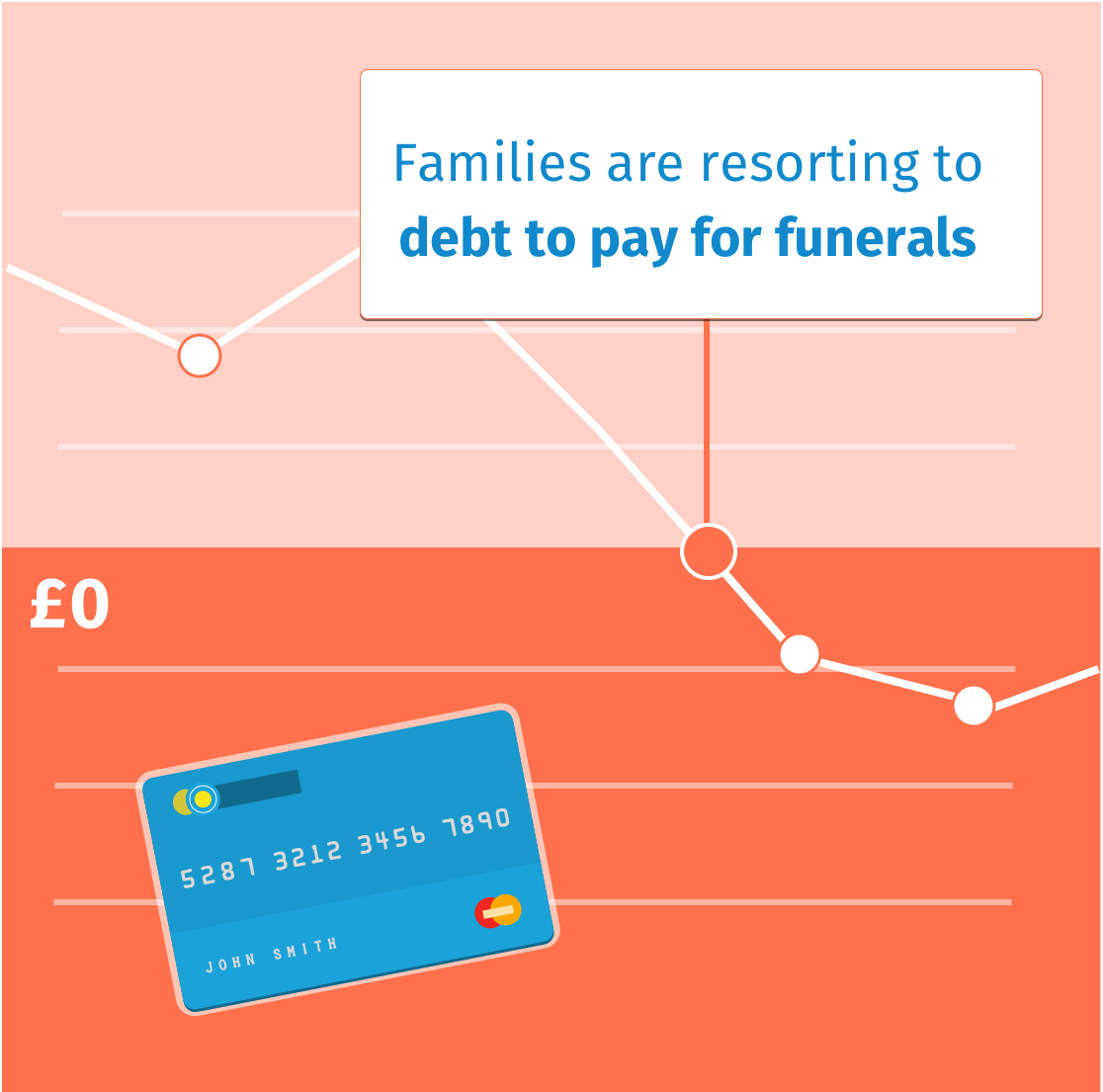

Looming debt crisis?

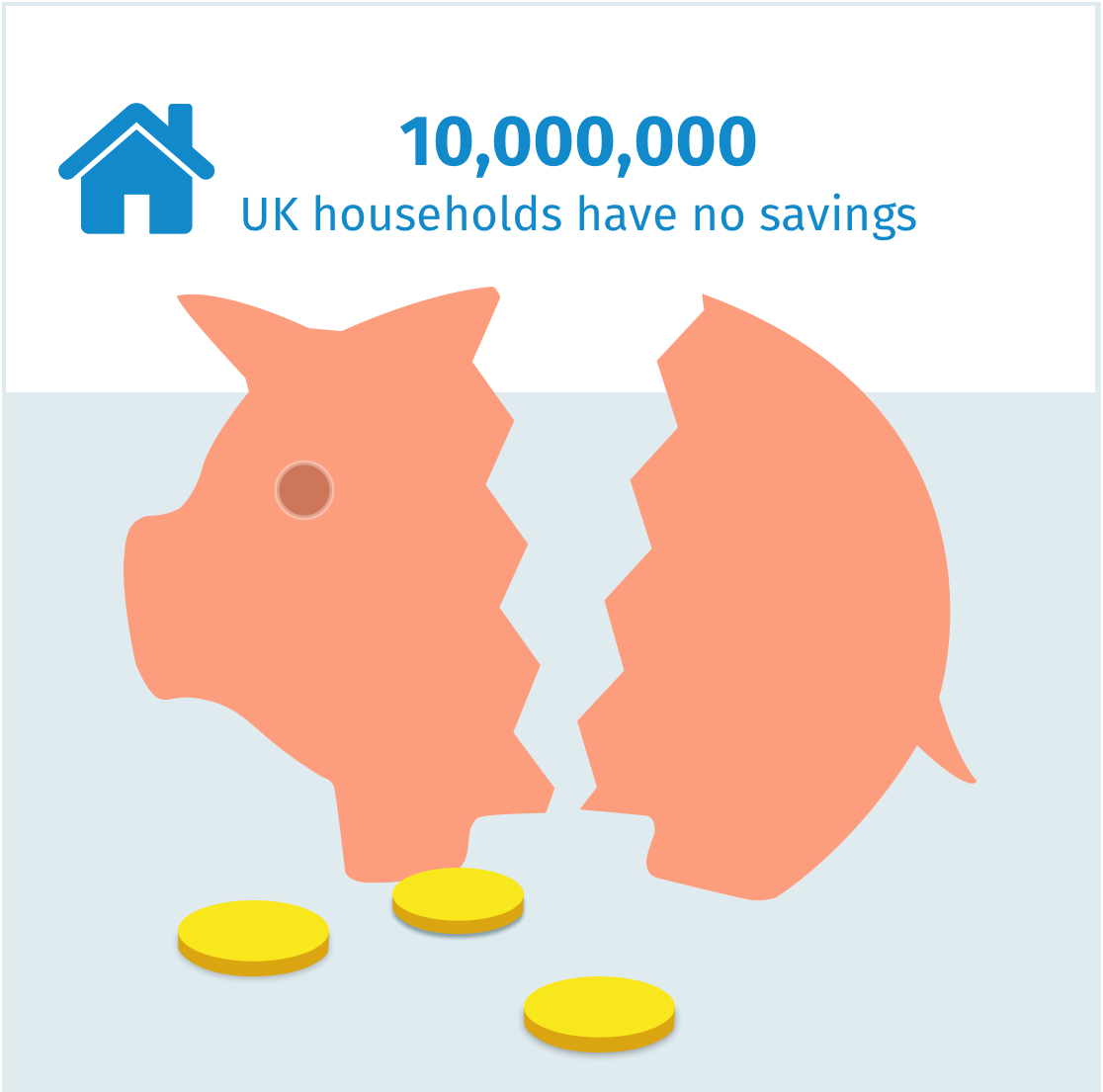

The average weekly income in the UK after tax is only £194, meaning families often have to resort to credit cards or personal loans to pay the considerable bill for a loved one’s funeral. With nearly ten million households in the UK having no cash savings, many poorer families could even face the nightmare scenario of having no money to lay their loved one to rest.

Importance of planning ahead

Planning ahead can be a smart financial move. By fixing your funeral costs at today’s prices you can potentially save your family thousands of pounds. Making your funeral arrangements in advance will also save your loved ones from the stress of planning your funeral at an already emotional time. They will know that all your wishes are being met and you are getting the send-off you would have wanted.